Scope: This guide helps first-time visitors, families, seniors, and winter-sports travelers choose and compare policy features for Japan. It explains medical, evacuation, CFAR, pre-existing condition waivers, natural-disaster language, and “cashless” treatment. It links to official resources—JNTO, the Embassy of Japan, JMA, and the UK FCDO—so readers can validate details and act with confidence. (Japan Travel, Embassy of Japan in the United States, jma.go.jp, GOV.UK)

Q: Is travel insurance mandatory for Japan?

No—visitors aren’t legally required to buy it, but authorities strongly recommend coverage. Japan’s tourism bodies note that some clinics may expect payment upfront unless the insurer can arrange cashless billing. Solid medical and evacuation benefits plus 24/7 assistance help navigate language, hospitals, and paperwork during emergencies. The safest move is to purchase before departure. (Japan Travel, Japan National Tourism Organization)

Q: What makes the “best travel insurance for Japan trip” in 2025?

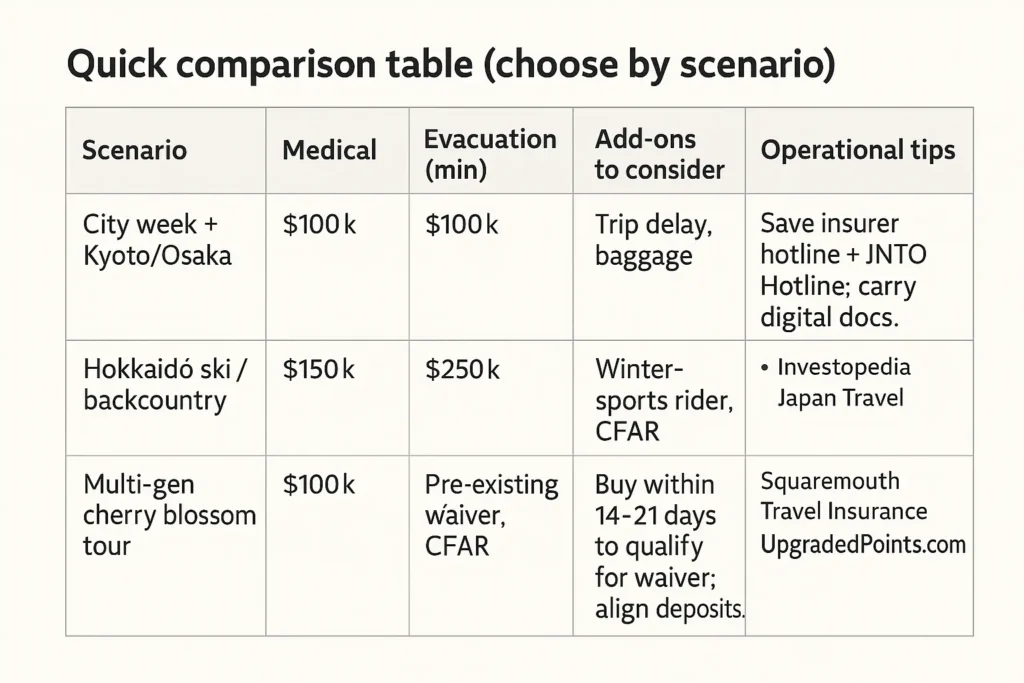

Look for high medical limits, robust evacuation, natural-disaster wording, and cashless treatment support. Many experts suggest at least $100,000 for medical and $100,000–$250,000 for evacuation, scaling higher for remote islands or ski areas. Policies with responsive assistance lines and clear claims steps reduce stress when minutes count. Compare benefits before price. (Investopedia)

Q: How do pre-existing condition waivers work?

Standard policies exclude pre-existing conditions, but many offer a waiver if bought shortly after the first trip payment. Insurers typically require purchase within 14–21 days and coverage of the full non-refundable cost with the same provider. Miss that window and the waiver is usually unavailable, even if you later upgrade. Read the timing rules carefully. (Squaremouth Travel Insurance, UpgradedPoints.com)

Q: What is CFAR and when is it worth it?

Cancel For Any Reason is an optional upgrade that broadens cancellation beyond “covered reasons.” Most issuers require purchase within 14–21 days of the first deposit, insure the full trip cost, and mandate cancellation a set number of hours before departure. Reimbursements typically run 50–75% of insured costs. It’s valuable for uncertain dates or high-demand seasons. (UpgradedPoints.com)

Q: How does “cashless” medical treatment work in Japan?

Cashless treatment means the clinic bills your insurer or its assistance partner directly, rather than charging you on site. JNTO explains this negotiated process and advises confirming your policy includes such services. The Embassy of Japan likewise encourages choosing plans that can coordinate hospitals, interpreters, and direct payments when possible. Always verify before you travel. (Japan National Tourism Organization, Embassy of Japan in the United States)

Q: What about earthquakes, typhoons, and weather disruptions?

Japan’s hazards include typhoons and quakes. A good policy names these perils, clarifies covered disruptions, and explains exclusions once an event becomes “foreseeable.” For situational awareness, monitor JNTO’s Safety Tips and the Japan Meteorological Agency’s Typhoon Center alongside your insurer’s alerts. Documentation from these sources can support claims when plans change. (Japan National Tourism Organization, jma.go.jp)

Q: How much should comprehensive coverage cost?

Pricing varies by age, trip price, and limits, but broad guidance places comprehensive premiums around 4–10% of the insured trip value. Expect to pay more for seniors, winter-sports riders, higher evacuation ceilings, or CFAR. A quick benchmark promotes budgeting without underinsuring high-risk portions like remote ski days or multi-city itineraries. (Investopedia)

Q: What if the traveler already has some credit-card protection?

Card benefits can help but often cap medical/evacuation too low and exclude pre-existing waivers or adventure sports. Standalone policies allow higher limits, cashless negotiation, and stronger disruption coverage. The prudent path is verifying exact card terms, then filling gaps with a dedicated plan that matches the itinerary’s risk profile and timing constraints.

Q: Which features matter most for different trip types?

City breaks need solid medical and evacuation plus trip delay protection. Powder hunters should add winter-sports coverage and higher evac limits. Multi-gen families often benefit from pre-existing waivers and CFAR for complex logistics. All travelers should bookmark the Japan Visitor Hotline for emergencies and translation help during care. (Japan Travel)

Q: Who should the traveler call in an emergency?

Call the insurer’s emergency assistance line first to open a case and confirm network facilities or cashless options. For additional help in English, Chinese, or Korean, Japan’s 24/7 Japan Visitor Hotline can provide guidance and referrals during incidents. Save both numbers in the phone and itinerary notes before departure. (Japan Travel)

Quick comparison table (choose by scenario)

Q: How should readers shortlist providers?

Start by mapping must-have features, then compare several quotes with identical trip costs and traveler ages. Prioritize policies that clearly state pre-existing waiver windows, evacuation ceilings, winter-sports definitions, and cashless assistance. Favor 24/7 hotlines and strong claims portals. Cross-check benefits rather than only price; hidden sub-limits can undercut protection when it matters. (Japan Travel)

Q: US companies to consider later (affiliate-ready)

Readers often evaluate Allianz Travel, Travel Guard (AIG), IMG, Seven Corners, Trawick International, World Nomads, and marketplaces like Squaremouth or InsureMyTrip to compare plans. Pair insurance with gear retailers (REI, Amazon) for medical kits and power banks, and tour platforms (Viator) to protect pre-paid activities with clear receipts for claims. (Squaremouth Travel Insurance)

References

- JNTO: Travel insurance in Japan; Safety Tips; Visitor Hotline (24/7). (Japan Travel, Japan National Tourism Organization)

- Embassy of Japan (USA): Insurance guidance and cashless treatment note. (Embassy of Japan in the United States)

- Japan Meteorological Agency: RSMC Tokyo Typhoon Center. (jma.go.jp)

- CFAR timing and mechanics; pre-existing waiver window. (UpgradedPoints.com, Squaremouth Travel Insurance)

- Typical cost benchmarks and coverage suggestions for 2025. (Investopedia)